Do you have a 401k or Individual Retirement Account? What fees lurk inside it? Do you put too much trust in a financial advisor to keep your best interests in mind? If you do have an advisor, are they truly an advisor? Or are they putting you into investments that are only serving them? Do you know how to spot hidden fees on your own to make your own decisions? Do you understand how to minimize investment fees to grow your wealth?

Fees have a negative impact on your ability to build wealth

Your savings rate, the percentage of money you save, is the largest contributor to your ability to build wealth. The returns on your investments are the next major contributor. Can you guess the third? Avoiding fees! And fees can be a major drag on your investment returns. To the tune of delaying your ability to retire by several years. Do you want to have to work an additional 3-5 years just because you paid more in fees? I didn’t think so!

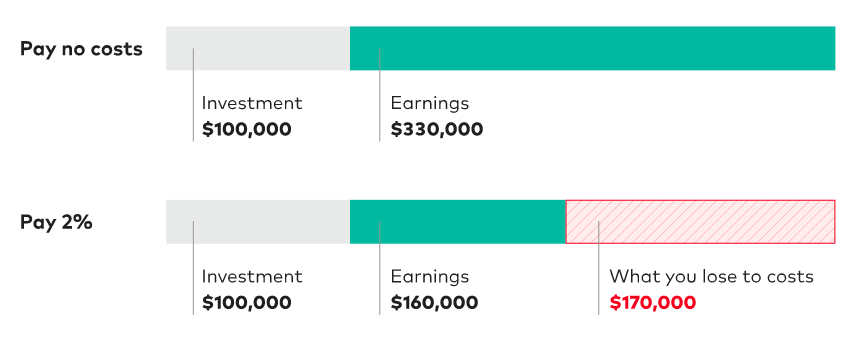

The chart below illustrates the drag that fees can have on your investments over time. In this example, $100,000 is invested and earns 6% annually in both scenarios (I realize this is lower than the historical returns, but bear with me). At the end of 25 years, the person in example one ends with $430,000. Person two, only $260,000. How does a 2% difference in fees become a 65% difference in the end? Because money is lost to fees (going to someone else) vs. going toward the actual investment (to you). The more you can maximize the amount going toward YOU vs. toward investment fees or advisor fees, the more you get to keep and the more your money compounds!

So, is your 401k or IRA really fee free? Spoiler alert, likely not!

I would venture to say that most people believe that the 401k provided by their employer is largely fee-free. After all, Fidelity, Vanguard and others offer fee-free trades. So, where do 401k companies make their money if everything trades for free? Well, the fees are largely built into the investments offered by the 401k provider. The fees charged come in the form of an expense ratio for the investment (mutual fund, index fund, bond fund, etc.). In the past, there were also a large number of mutual fund companies charging a front load, which is an extra commission on top of the ongoing expenses of the fund. The horrible part is that these higher-rate managed funds largely have not delivered the value and returns offered by low-cost index funds.

What’s the difference between a mutual fund and an index fund?

A mutual fund is a managed fund, meaning that there are people at the investment company picking and choosing a set of stocks to offer within the fund. An index fund, on the other hand, is not actively managed. It generally follows the market or market sector it is connected to, and there’s no active trading of individual stocks within the fund. For instance, an S&P 500 index will follow the direction of the overall S&P. A small cap index will follow the performance of only smaller companies, but overall fees for index funds are less costly than fees for mutual funds. As you can see below, mutual funds have fees that are nearly 12X higher than those of index funds. And most of the time, index funds beat mutual funds in performance in the long run.

| Mutual Fund | Index Fund |

| Actively managed | Not actively managed; follows the overall market |

| Higher fees (average 0.71%) | Lower fees (average 0.06%) |

| Wide array of investments available | Wide array of investments available |

The hidden fees of target date mutual funds

Target date funds have brought a solution to many investors who seek a hands-off approach to their retirement and other investment accounts. These mutual funds include a mix of stocks, bonds and other investments that gradually move from aggressive toward conservative as the fund reaches its ‘target date.’ For instance, a 2040 target date fund would offer a larger mix of stock than bonds in the beginning, but gradually shift over time as the year 2040 approaches. Typically, a person chooses the date that is closest to their intended retirement date. A growing number of employers offer these funds as part of their 401k plans and often use target date funds as the default investment if the employee chooses to make no election.

Most people do not realize, however, that many target date funds are double-dipping on fees. Target date funds are a bunch of funds packaged up and sold as a fund with a target retirement year on it. Let’s take the Fidelity Freedom Fund 2040 (FFFFX) for instance. The expense ratio on this fund is 0.75%. Well, this fund includes a pile of Fidelity’s other funds….including mutual funds, all which have separate expense percentages in addition to the 0.75% mentioned above. And unfortunately, not all of the expenses are included in the 0.75%. If the fund manager decides to buy and sell other non-Fidelity securities within the fund, those are not included in the expenses quoted above. Pretty transparent, huh?

Here’s an example of language from T. Rowe Price within their prospectus on their 2040 target date fund (which quotes a 0.6% expense ratio):

“On October 1, 2022, the all-inclusive management fee rate was 0.60%. The management fee is calculated and accrued daily, and it includes investment management services and ordinary, recurring operating expenses, but it does not cover interest; expenses related to borrowings, taxes, and brokerage; nonrecurring, extraordinary expenses; and acquired fund fees and expenses. Rule 12b-1 fees applicable to the Advisor Class and R Class are also not covered by the all-inclusive management fee. In addition, T. Rowe Price receives management fees from managing the underlying funds, and Price Investment Management, Price International, Price Hong Kong, Price Japan, and/or Price Singapore may receive a portion of the management fee that T. Rowe Price receives from those underlying funds for which it serves as investment subadviser.”

These additional ‘hidden’ expenses end up reducing the return rate of the fund, thus lowering how much you make on the investment. Expenses end up buried in the paperwork that most investors never read.

3 key tips to avoid the fees that are slowing your wealth growth

1. Check the fees on each of your investments.

It is very important to review the fees on each of your investments in your account. You want to ensure that you minimize investment fees as much as possible. I suggest using a site such as morningstar.com to plug in each one of your investments to understand the expense ratio associated with it. If you have an advisor, don’t take their word for it. Look the expenses up for your investments yourself to verify. I provided expense averages above (0.71% for mutual funds and 0.06% for index funds). If your investments are larger than that. Really, anything over 1%, take a closer look and evaluate that investment. If you have an advisor, question why they put you into an investment that has a higher-than-average fee.

2. Consider ultra-low fee index funds vs. mutual funds

As mentioned earlier, index funds are much cost-effective investments that will help you minimize investment fees. And they more times than not outperform actively managed mutual funds. According to the New York Times, over a full 20-year period ending last December 2022, fewer than 10 percent of active U.S. stock funds managed to beat their benchmarks. Even multi-billionaire Warren Buffet (arguably the best stock picker ever) has instructed in his estate that the money for his family be invested in a low-cost S&P 500 index fund.

3. If you have an advisor, determine if they’re truly adding value

If you’re investing in low-maintenance, low-cost index funds, you might begin questioning whether you even need a financial advisor. Are they adding any incremental value? Many advisors charge a percentage of assets under management, such as 1% annually of your overall portfolio of investments. I personally think that is a tough pill to swallow, especially because most of my portfolio is index funds. A certified financial planner who charges by the hour and helps you more broadly with your entire personal finance picture, on the other hand, might be worth talking to periodically. A good hourly fee advisor will help you minimize investment fees.

In closing, minimize your fees to minimize what you lose and maximize what you keep

Fees are a huge drag on your ability to grow your wealth. Defend your dollars by ensuring that you understand what fees are occurring in your investments, and take action to minimize the fees before it is too late. It will be ‘Good for Your Wealth.’