There has been a lot happening over the past several months which may have you concerned – Russia’s intensifying attack on Ukraine, inflation and the continued uncertainty of “WTF is next with the COVID-19 pandemic” just to name a few. When unexpected events occur, it certainly has a human impact. But, it can also leave you worried about your finances and your future. It is important to prepare financially for uncertain times.

The good news is that with careful financial planning, you will be better prepared to weather the storm during turbulent times.

Have an investment mission or plan and stick to it.

In order to avoid making hasty decisions when emotions are high during an event, it is important to have an investment mission or plan. For example, many people decide on a mix of investments as part of their plan, based on their age or risk tolerance. One popular rule of thumb is holding a percentage of stocks equal to 100 minus your age. I personally take a bit more of an aggressive approach and take 110 minus my age. For someone who is 40 years old, the “100 minus age” rule would mean 60% stocks and 40% bonds or other income-type investments. It is really a matter of your risk tolerance and when you think you need the money. This is why it is called a rule of thumb. The idea is that as you get older, you become less risk tolerant. By shifting from stocks over time to more stable investments, it helps to smooth out the ups and downs.

As part of my personal plan, I not only cover what kind of mix I want, but I also outline when I will re-balance my portfolio. I do this twice per year. It is one big thing you should do to prepare financially for uncertain times.

Keep your investment portfolio balanced to prepare financially for uncertain times.

Your investment portfolio, if you have one, is likely made up of a number of different types of investments. This could include stocks, bonds, real estate and other investments. To ensure you do not overexpose yourself to risk, you need to re-balance your portfolio of investments regularly. Let’s say, based on your age and risk tolerance, you have 80% of your portfolio in stocks or a stock index fund, and the remainder in bonds. Over the year, the stock market goes gangbusters and stocks now make up 90% of your portfolio. Re-balancing means that you bring your portfolio back to 80/20 by selling off some of that stock and buying more bonds to stay at that 80/20 level. By re-balancing, you’re maintaining your level of risk tolerance with time and also smoothing out the ride along the way. It ensures that one particular investment type doesn’t take over your portfolio, exposing you unknowingly to additional risk.

Avoid panic selling. Don’t time the market. Stay the course.

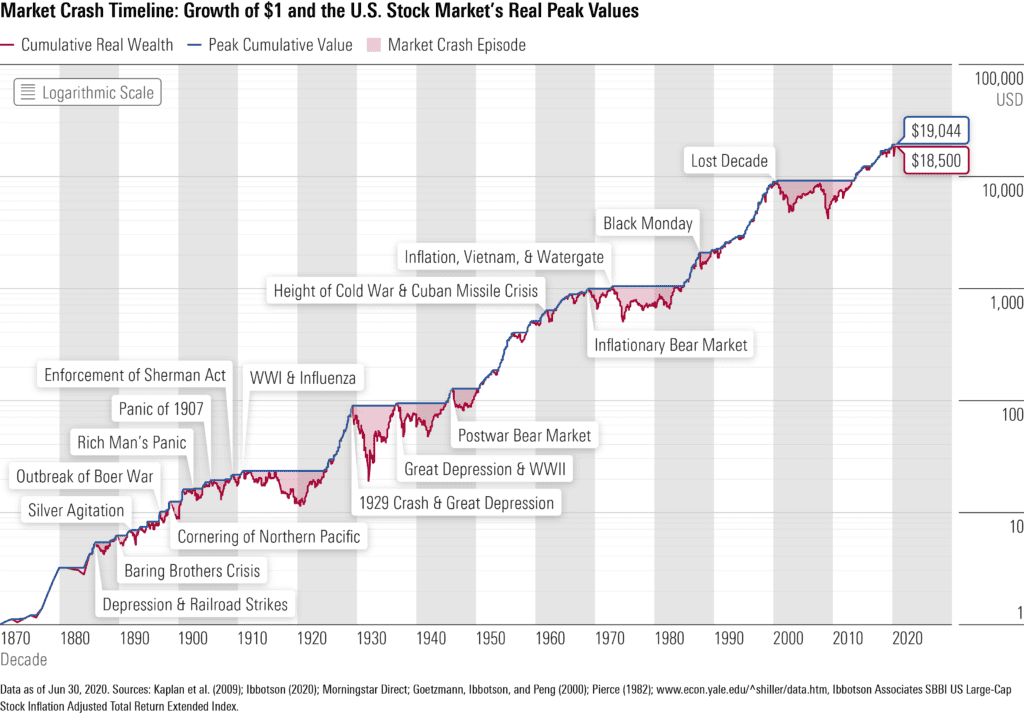

When it comes to your investments, toss the fear aside in favor of playing offense. Even when the market is down, you have not lost unless you sell the investments. Back during the 2008 stock market crash, I heard several stories from friends and relatives who “sold everything” as the market was crashing. They acted on emotion, specifically fear. The beauty of the stock market is that it always goes up over time. Sure, it has ups and downs along the way, but it always goes up. See the chart below which shows all of the market crashes over the past several decades. As you can see, the chart illustrates overall growth of $1 in the market over time. By having a plan in place, you will avoid the temptation to panic sell. When you sell during a downturn, you are locking in losses. The worst part is that it will be hard to determine when to get back into the stock market. You should never try to time the market.

When the market is down, consider it bargain shopping time.

Although I don’t “time the market,” I do often buy on the dips, when the market is down. If you have funds available, by investing during down times, your overall portfolio will benefit as things start coming up. Warren Buffet, the world-renowned billionaire value investor, buys solid companies that are dealing with difficult times. He knows that dips in the market are only temporary, so he puts his money to work by buying quality investments when they are “on sale” at bargain prices. I very much admire Mr. Buffett.

The 2008 recession had a negative impact on many, including me and my wife. But, the silver lining was that my wife and I were able to reset our priorities away from a large home and into investing. By piling extra savings into investments (mostly low-cost index funds) during the bottom of the market, as things shot up over the following decade and beyond, it allowed wealth to accumulate.

“Be fearful when others are greedy and greedy when others are fearful”

Warren Buffett

Get an emergency fund. If you have debt, work toward paying it off.

To reduce your financial risk and prepare for uncertain times, it is important to have an emergency fund of a minimum of 3-6 months of living expenses saved. If you do not have an emergency fund, work on accumulating that first. This will keep you from having to sell your investments in a down market when things are rough in order to cover your living expenses.

Then, if you have debt (especially consumer debt), take any additional funds you have and pay down that debt as quickly as you can. When there could be rocky times ahead, one of the best things you can do is prepare by minimizing any debt and monthly payments you have which would end up being a huge burden if your income decreased. This will ensure that if you lose a job, your emergency fund will go further if it needs to. When times are good, they’re good. But when they’re bad, they can be pretty bad. If you are someone who has taken on a lot of debt during these good times over the past decade plus, work on getting the debt paid down to lower your risk.

Minimize your exposure in speculative investments. Consider low-cost index funds.

If you are concerned with losing money, avoid speculative investments…or at least limit your exposure. I’ve heard lots of stories of people putting half of their savings into cryptocurrency or into single investments, such as Tesla. I have also seen people putting lots of money into the stock of the company they work for. This is overexposing yourself to unnecessary risk. If you buy a large amount of stock in the company you work for, you are putting all of your eggs into one basket.

Currently, Tesla’s stock price puts the company at a value of 5 times that of GM, Ford and Stellantis (Chrysler) combined! I realize Tesla has a lot going for it, but I think there is a lot of hype at play as well. This is why I rarely purchase individual stocks, such as Tesla. When I do purchase individual stock, I only invest a small portion of my portfolio in them – roughly 5%. Because I invest in broad stock index funds (such as U.S. total stock market index), I own Tesla…and many other companies of varying sizes. And if one of those companies were to go completely bankrupt, it wouldn’t lead to my financial demise as well. It would be a much smaller impact as part of that broader index fund. Limiting your exposure to speculative or risky investments will help to prepare financially for uncertain times.

Remember, slow and steady wins the race

I get it. It is very difficult to see things happening and not react emotionally. By playing offense, it will reduce the likelihood of making hasty decisions and losing out financially in the long term. By going for the long play with your finances and adopting that frame of mind, you will be less likely to react to what really amount to short-term issues. Make a plan, stick to it, and check on it periodically. It will be ‘good for your wealth’ at the end of the day.

1 Comment

Katie Fenster · March 22, 2022 at 9:20 pm

Very helpful information! I love your blog!

Comments are closed.